Employee Benefits

What the One Big Beautiful Bill Act Means for Employee Benefit Plans

On July 4, 2025, President Donald Trump signed into law the One Big Beautiful Bill Act (OBBB Act), a sweeping piece of tax and spending legislation that carries significant implications for employee benefits. For HR professionals, business owners, and benefits administrators, understanding the changes this law introduces is essential as many of its key provisions take effect starting in 2026.

Key Takeaways:

- Expanded HSA eligibility including ACA bronze and catastrophic plans.

- Telehealth exception for HDHPs is now permanent.

- Higher annual limits for dependent care FSAs.

- Student loan repayment benefits extended beyond 2025.

- Education assistance benefits now adjusted for inflation.

- New child savings vehicle introduced—called Trump Accounts.

Expansion of Health Savings Account (HSA) Eligibility.

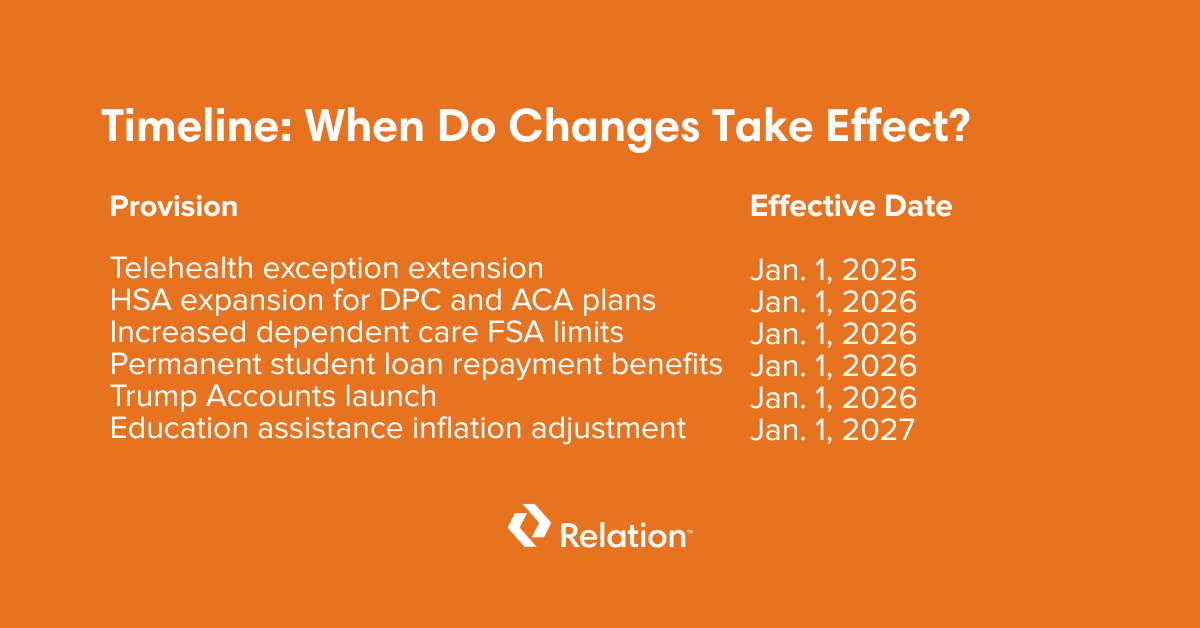

One of the most substantial changes brought by the OBBB Act is the expansion of Health Savings Account (HSA) eligibility. Effective January 1, 2026, individuals participating in direct primary care (DPC) arrangements can contribute to an HSA, provided their monthly DPC fees are $150 or less for individuals, or $300 or less for families. These thresholds will be indexed annually for inflation. DPC arrangements, which involve paying a flat periodic fee for access to primary care services, are growing in popularity, and under the new law, these fees can now be treated as qualified medical expenses payable with HSA funds.

In addition, the OBBB Act broadens HSA accessibility within the individual insurance market by categorizing all bronze and catastrophic plans offered through ACA Exchanges as high-deductible health plans (HDHPs). This reclassification allows more individuals who purchase insurance on their own to become eligible for HSAs.

Permanent Telehealth Exception for HDHPs.

The pandemic temporarily allowed HDHPs to cover telehealth services pre-deductible without disqualifying HSA eligibility. The OBBB Act makes this telehealth flexibility permanent for plan years beginning after December 31, 2024. This move is expected to encourage continued growth in virtual care offerings and remove barriers for employees seeking more accessible and affordable healthcare.

Increased Limits for Dependent Care FSAs.

Employers offering dependent care flexible spending accounts (FSAs) will also need to take note of new limits established by the Act. Beginning in 2026, the maximum annual contribution will increase to $7,500 for single individuals and married couples filing jointly, and to $3,750 for married individuals filing separately. These higher limits provide employees with additional tax-free savings opportunities to cover eligible childcare and dependent care expenses, although it’s important to note that these amounts are not indexed for inflation and will remain fixed unless amended by future legislation.

Extended Student Loan Repayment Benefits.

The OBBB Act also brings good news for employees with student loan debt, offering a powerful retention and recruiting incentive, particularly for Millennial and Gen Z employees. Originally set to expire after 2025, the OBBB Act permanently extends the ability for employers to pay down employees’ student loans using educational assistance programs. Employers can continue to contribute up to $5,250 annually toward employees’ student loans on a tax-free basis. Starting in 2027, this $5,250 limit will be adjusted each year for inflation, allowing employers to offer increasingly meaningful benefits to workers who are burdened by educational debt.

Introduction of “Trump Accounts” for Children.

One of the more novel introductions in the OBBB Act is the creation of “Trump Accounts,” a new type of tax-advantaged savings vehicle for children under the age of 18. Set to take effect in 2026, these accounts function similarly to individual retirement accounts (IRAs), with earnings growing tax deferred. The annual contribution limit is set at $5,000 per child, with inflation adjustments beginning in 2028. Children born between 2025 and 2028 may also be eligible for a special $1,000 federal contribution, providing an extra incentive for families to participate. Employers may make tax-free contributions of up to $2,500 per year to these accounts on behalf of an employee’s child or dependent, with these contributions also subject to future inflation adjustments. Employers offering Trump Accounts will need to create a written plan document and follow rules similar to those governing dependent care FSAs, including nondiscrimination testing and employee communications.

Next Steps.

The various changes introduced by the OBBB Act reflect a clear shift in policy aimed at expanding access to healthcare, supporting working families, and incentivizing financial security for the next generation. While the benefits are significant, the administrative responsibilities will also grow. Employers should begin planning now.

- Review your benefits strategy with HR and legal teams.

- Update written plan documents before the 2026 effective dates.

- Communicate changes clearly to employees.

- Explore adding Trump Accounts and HSA-eligible plans to your offerings.

Proactively adapting your benefits package can give your organization a competitive advantage in recruiting and retaining talent.

If you need help navigating these changes, consult with your benefits advisor or legal counsel to stay compliant and maximize the impact of these new employee benefit provisions.