Since the pandemic, the shift toward digital operations in the business world has become a vital evolution. However, with the many benefits of a connected, online enterprise comes a slew of risks that traditional insurance packages, such as Business Owner’s Policy (BOP) Coverage Insurance, may not address. This gap has led to the increasing importance of Cyber Insurance for businesses, and it’s time you find an insurance broker who understands this is a crucial aspect of modern insurance coverage.

Why Is Cyber Insurance Important?

A 2022 Official Cybercrime Report by Cybersecurity Ventures predicted the global annual cost of cybercrime would reach $8 trillion in 2023—an amount greater than the annual GDP of every nation on Earth, barring China and the United States. And the cost of cybercrime isn’t expected to slow down, with damages projected to reach $10.5 trillion by 2025. Along with significant financial losses, businesses of all sizes may suffer reputational harm and lawsuits from affected customers.

How Misconceptions About BOPs Can Affect Insurance Brokers

Many businesses erroneously think that cyber threats are already covered under their BOP. But what does a Business Owner’s Policy cover? Typically, BOP Coverage Insurance addresses property damage, liability, and other conventional business risks. Cyber threats often fall outside this umbrella.

The Real Cost of a Cyberattack

The real cost of a cyberattack might surprise you. While CNBC reports the average cost of a cyberattack is $200,000, Business.com says the average cost of a data breach to a small business ranges from $120,000 to $1.24 million. Whatever the number, these can feel like abstract stats that don’t really apply to your business.

So, here are a few real claims examples we know of that might bring it closer to home:

- An online retailer went offline for six hours due to a cyberattack on the data center that hosted their site. The cost of recovering the website, lost revenue, and incident response expenses was $144,000.

- A public relations firm was hacked, and its system was infected with malware. IT forensics, legal, and notification costs were $50,000.

- A law firm had $118,830 fraudulently transferred overseas by cybercriminals posing as the firm’s bank.

- An employee in a manufacturing company clicked on a malicious link in an email, infecting the system with malware and encrypting all data. Incident response and recovery costs totaled $60,000.

Fortunately, all the above had cyber liability insurance so those costs and losses were covered. But without a policy, each company here would have been responsible for every dollar.

Is Your Company Covered For A Cyberattack?

Cybersecurity has now become a necessity for every business that uses technology. Could your company afford to pay the above costs or lose revenue due to downtime while you figure out how to respond to a cyberattack? With cyber liability insurance, you wouldn’t have to.

We can work with you to find what coverage best fits your needs. We’ll walk you through the process at every step to ensure your bottom line is protected and you have the resources to respond in case you are targeted.

Call one of Insurance experts today to make sure your business is protected from Cyber Threats.

April Is Distracted Driving Awareness Month. The National Safety Council recognizes April as Distracted Driving Awareness Month to help raise awareness about the dangers of distracted driving and encourage motorists like you to minimize potential distractions behind the wheel. Learn more on ways you can help prevent distracted driving.

Distracted Driving Overview

According to the Centers for Disease Control and Prevention, distracted driving refers to any activity that may divert a motorist’s attention from the road. There are three main types of distractions that can interfere with drivers’ attentiveness behind the wheel, including:

Visual distractions

These distractions involve motorists taking their eyes off the road. Some examples of visual distractions include reading emails or text messages, focusing on vehicle passengers, looking at maps or navigation systems, and observing nearby activities (e.g., accidents, traffic stops or roadside attractions) while driving.

Manual distractions

Such distractions entail motorists removing their hands from the steering wheel. Key examples of manual distractions include texting, adjusting the radio, programming navigation systems, eating, drinking or performing personal grooming tasks (e.g., applying makeup) while driving.

Cognitive distractions

These distractions stem from motorists taking their minds off driving. Primary examples of cognitive distractions include talking on the phone, conversing with vehicle passengers or daydreaming while driving.

Regardless of distraction type, distracted driving is a serious safety hazard that contributes to a significant number of accidents on the road. In fact, the National Highway Traffic Safety Administration reported that more than 2,800 people are killed and 400,000 are injured in crashes involving a distracted driver each year—equating to approximately eight deaths and 1,095 injuries per day. Considering these findings, it’s crucial to take steps to prevent distracted driving.

Distracted Driving Prevention Tips

Whenever you get behind the wheel, keep these distracted driving prevention measures in mind:

- Put away your phone. Silence your phone and store it in a location that is out of reach while driving to lower the temptation to check it.

- Plan your trip before you leave. Program your navigation system prior to hitting the road to get familiar with your journey and feel confident in your route.

- Don’t fumble with your playlist. Select a radio station or plug in a predetermined playlist before driving to limit the need for music adjustments.

- Secure passengers. Ensure kids are properly situated in car seats (if needed) with seat belts fastened. Keep pets stationary in the back seat.

- Avoid multitasking. Never complete additional tasks—such as eating or personal grooming—behind the wheel.

- Stay focused. Concentrate your mind on the road by keeping distracting conversations to a minimum and looking straight ahead.

This article is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel or an insurance professional at Relation Insurance for appropriate advice.

©2023 Zywave,Inc. All rights reserved.

Recent market developments have demonstrated signs of an improving commercial insurance landscape. Yet, industry experts asserted that ongoing headwinds facing certain lines of coverage will continue to generate hardened conditions overall, therefore driving up premiums. As such, it’s essential for businesses to be aware of the following market trends and how they may impact coverage costs:

Labor shortages trends impacting commercial insurance costs

The last few years have seen widespread labor shortages, largely stemming from employees adjusting their job priorities in response to the COVID-19 pandemic. Such shortages have motivated some businesses to hire less experienced workers and place extra demands on existing employees to fill labor gaps; however, doing so can heighten liability exposures and increase the risk of workplace accidents, paving the way for rate jumps in several commercial insurance segments.

Supply chain disruptions trends impacting commercial insurance costs

Continued pandemic-related challenges, global transportation breakdowns and commercial driver shortages have slowed shipment and delivery times for many high-demand goods, creating supply chain issues for businesses across industry lines. These issues have led to considerable disruptions, prolonged recovery times, compounded claim expenses and elevated premiums in multiple commercial insurance segments.

Inflation issues trends impacting commercial insurance costs

In recent years, labor shortages and supply chain issues have fueled rising inflation concerns throughout the commercial insurance space, as evidenced by a surging consumer price index (CPI). Altogether, the elevated CPI has driven up claim costs, inflated total loss expenses and prompted rate hikes for various lines of coverage.

Recession risks trends impacting commercial insurance costs

Some economic experts have forecasted that the United States is headed toward a recession in the near future. During a recession, businesses usually experience decreased sales and profits, which may cause them to reduce their workforces and cut their spending to help maintain financial stability. Although having fewer employees could minimize occupational injuries and associated claims, limited funding for risk management and cybersecurity initiatives may create further liability exposures, making busi- nesses more vulnerable to increased losses and higher commercial insurance premiums.

Social inflation trends impacting commercial insurance costs

Social inflation refers to societal trends that push insurance costs above the overall inflation rate. Current drivers of social inflation include increased third-party litigation funding and the rise of anti-corporate culture. Amid these trends, businesses have been held more ac- countable for their wrongdoings, sometimes resulting in nuclear verdicts (jury awards exceeding $10 million). Social inflation has been a main factor in rising claim severity and rate jumps across many commercial insurance segments.

Extreme weather events impacting commercial insurance costs

Natural disasters (e.g., hurricanes, tornadoes, hailstorms and wildfires) continue to make headlines as they become increasingly devastating and costly. Making matters worse, these events aren’t limited to one geographic area; they impact establishments across the United States. Natural disasters have left businesses with significant repair and re- placement expenses, exacerbating losses and resulting in higher commercial insurance premiums.

During these challenging times, we are here to provide much-needed market expertise. Contact us today for additional risk management guidance and insurance solutions.

This article is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel or an insurance professional at Relation Insurance for appropriate advice.

©2023 Zywave,Inc. All rights reserved.

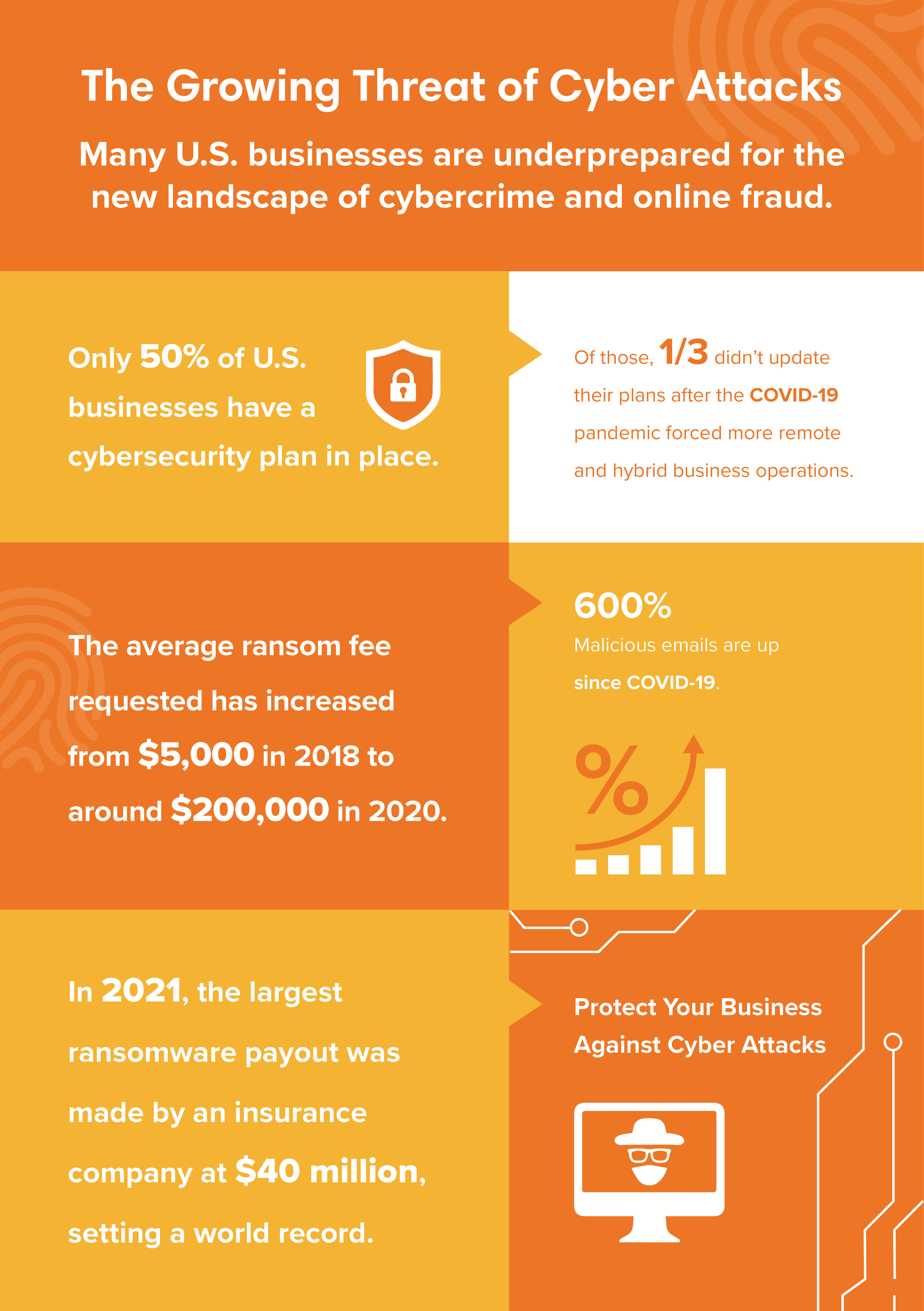

October is National Cybersecurity Awareness Month, and as the world grows digitally, cybercrime and online fraud are becoming more complex. Our experts have put together a helpful guide for you to assess your cyber risk and whether you may need to update your cybersecurity plan in order to protect your business against cyber attacks.

Do you have a cybersecurity plan in place?

Only half of all businesses in the United States have a cybersecurity plan in place – a shockingly low proportion, considering that cyber attacks do not discriminate. Every business, large and small, is a target. If you do not have a plan in place, now is the time to create one. (If you’re not sure where to start, you can reach out to a cybersecurity specialist for a free consultation!)

When was the last time you updated your cybersecurity plan?

Of the businesses that have a plan for cybersecurity, a third have never updated their plans after the increase in remote and hybrid work operations that came with COVID-19 in 2020. At a time when exposure and risk is rising exponentially, it’s imperative to revamp your cybersecurity plan. Experts recommend reviewing and adjusting your plan at least once per year to protect your business against the latest malware and cyber attack strategies.

How do you keep your team aware of online threats that could put your business at risk?

Malicious emails have increased a whopping 600% since 2020. At the same time, ransomware is becoming more aggressive, with the average requested fee going from $5K in 2018 to $200K in 2020. It only takes one slip-up by a well-meaning team member to take down everything you’ve worked so hard to build. Make sure your whole team is educated on what cyber threats can look like and what to do if faced with a potential risk.

How does your website expose you to risk?

As cybercrime evolves, it’s important to know how your website holds up against current threats. Through our cybersecurity team and partners, we can put your site to the test against potential threats, so you can know where you stand, and we can work together to mitigate your risk.

What cyber protection is common practice for your industry and company size?

Discover how your competitors and others in your industry are protecting themselves. Using our cyber protection partner’s benchmarking tool, we can review the typical coverage of your industry for a company your size, so you’ll know exactly how you stack up.

What is your existing cyber liability, and which coverage is right for your business?

That’s what we’re here to help you find out. When you work with us to manage your cyber risk, our cybersecurity experts and partners analyze and assess the entirety of your cyber risk and build a custom program from the ground up. Our goal is to protect what you’ve built.

Cyber risks aren’t going away. But we’re here to help. We believe every business should be protected and our team is ready to partner with you to ensure your business has what it takes to stay safe online.

Contact our Cyber Security experts for a free consultation and protect your business against cyber attacks.

[hubspot type=”form” portal=”7375193″ id=”fc505768-dc0c-4d81-942d-d86c55a59363″]

For trucking and transportation companies, managing insurance isn’t for the faint of heart. Premiums are on the rise, legal settlements are increasing, and equipment is getting more expensive. In addition, new rules and legislation are changing how safety is understood and measured. As the landscape shifts, technologies that help put driver safety at the forefront are playing a key role in reshaping the industry, and also allowing technology-adapters to reduce risks and position themselves more in the driver’s seat.

Understanding Increased Premiums

Trucking insurance premium increases—combined with increases in climbing equipment costs, driver pay, and, recently, fuel—are putting pressure on trucking companies to reduce expenses where they can. According to the American Transportation Research Institute (ATRI), the average carrier cost per mile for truck insurance increased from $0.064 in 2013 to $0.075 in 2017, and the Wall Street Journal found “The cost of truck insurance premiums rose 12%, on average, to 8.4 cents a mile, in 2018 from the previous year.”

Here’s a couple of reasons why premiums have been increasing for years for trucking companies:

Nuclear Verdicts

The severity of claims fueled by nuclear verdicts—settlements that range in the millions—has increased dramatically in recent years. The enlarged size of jury awards and settlements can partly to attributed to the increased frequency of court cases referencing data from FMCSA’s Compliance, Safety, Accountability (CSA) program.

CSA data is used to identify motor carriers with safety issues and prioritize them for warning letters, interventions, and/or investigations. The data is updated monthly and is organized into seven categories, known as the Behavior Analysis and Safety Improvement Category scores (BASICs). Five of the seven BASICs are publically available online through FMCSA’s Safety Measurement System. (Congress removed some CSA data from public view in December 2015—including the Crash Risk Indicator and Hazardous Materials BASICs—due to concerns about the data accurately portraying carrier performance.)

With BASIC scores like Hours of Service, Unsafe Driving, and Vehicle Maintenance openly accessible, lawyers can use compliance history in combination with accident details to try to establish negligence in a court of law. This strategy can result in high jury verdicts and defense costs.

As a result, claims that might have been $200,000 five years ago have risen to $500,000 in some cases. Significantly higher settlements, jury verdicts, and fear of potential jury verdicts have increased reserve forecasts, which in turn have had a direct effect on defense costs and insurance premiums. Premiums that may have averaged $6,000- $7,000 earlier in the decade can now run 20-50% higher, especially if the voluntary insurance market continues to decline and State Assigned Risks programs are the only takers.

Some companies believe the factors that contribute to BASIC scores have no direct correlation to how safe they are as a company. Although the CSA scoring is not perfect, the methodology is directionally accurate and typically the motor carriers that complain about their scores do not perform as well as their competitors. When carriers choose not to invest in safety policies and proven safety technologies, it is arguable that profitability is being placed ahead of safety, which can further increase litigation costs.

CSA Scores Changing to More “Rigorous” Data-Driven Model

Currently, the Federal Motor Carrier Safety Administration (FMCSA) uses CSA scores as the primary means to identify high-risk motor carriers. But a new statistical model—the IRT model—being explored by the FMCSA would utilize data to measure a motor carrier’s “safety culture,” rather than attempt to predict its likelihood of a crash, according to a piece in Transport Topics. However, it has been widely reported that FMCSA officials will not make a decision until September 2020 about whether to adopt the IRT model, which is complex and may be difficult to explain to the trucking industry.

In this litigious environment, carriers that choose to invest in safety technology and embrace statistical models will have more data-driven resources to help try to dissuade claimants from landing a lottery-type award.

Improving Safety Proactively

Instead of just going along for the ride, trucking companies can consider taking matters into their own hands by investing in technologies that can help substantially reduce risks, as well as gathering data that can reinforce a culture of safety. In many cases, the cost of avoiding one nuclear verdict may offset, or even pay for the investment. Here are a few of the most popular safety technologies being implemented by trucking companies:

- Dash Cams: Dashboard cameras on trucks are becoming table stakes and have already been positively reducing premiums. In some cases, cameras can completely eliminate a possible accident claim which would had been a difficult “he said / she said” battle in the past. Even in the case of a head-on collision, dashboard cameras simplify determining who is at fault. An easy video review process can even exonerate a driver on the spot.

- Collision Avoidance Systems: Smart anti-collision technologies that sense when a vehicle is getting too close, and apply the brakes on behalf of the driver, are already mitigating risks. While the technology has been around for several years, more 2020 rigs promise to come equipped with this technology already in place, and other retrofit options have recently come to market for older trucks. These technologies don’t just help drivers avoid accidents; they also lay the foundation for safer practices by collecting data that can be used to retrain drivers, or to create full driver safety programs for a company to make the entire fleet safer. While equipping rigs with collision avoidance technology may cost $30,000-$50,000 extra, with fewer collisions, diminished severity of claims, and more affordable premiums, the dividends can pay off down the road.

- Anti-Fatigue Technology: A slew of innovative new technologies are beginning to hit the industry to help diminish driver fatigue. While dash cams can retroactively show whether a driver was asleep at the wheel in the event of an accident, predictive technology can reduce the likelihood of dangerous scenarios. For example, fatigue meters technology uses hours-of-service logs to predict driver fatigue levels, updating managers with thorough assessments for every driver in the fleet. Wearables (like a Fitbit-like device) are similarly analyzing fatigue by measuring body movements, assessing sleep quantity, and predicting when alertness will start to decline. Even facial mapping technologies that look for symptoms of fatigue from a driver’s face, such as yawning or head nodding, can estimate driver alertness.

Data gathered from these new safety technologies can not only help identify and sideline potentially dangerous or fatigued drivers, but also help lead to more personalized training and hours-of-service regulations for each driver to increase safety.

It’s been said that you can’t stop progress. In this case, technology has come to the trucking and transportation industry. While retrofitting trucks with safety-centered technology or buying new trucks with technology already installed can seem expensive and arduous for many industry veterans, encouraging a safety-centered culture that protects drivers can pay off in the long term in the form of reduced accidents (and lawsuits), as well as lower premiums. Those in the industry quickest to embrace a safety-first mentality and support it with the best tools and protocols currently available will be ready to evolve and be more attractive to potential employees.

Peter Smelzer, AAI, AIS is a Fleet Risk Advisor for Relation Insurance Services. He can be reached at [email protected] or on LinkedIn.

An annual review of your insurance coverage may be the time to make changes in coverage, endorsements, or carriers.

Any time you make changes in the way your business runs, you can also change your exposure to risks. As your organizational needs evolve over time, it’s a good business practice to consider whether there are other carriers that can offer reduced premiums or expanded coverage better suited to your requirements as you grow, move, or expand your offerings.

Fortunately, the insurance marketplace is responsive to changing risks that buyers face. In some cases, it may make more sense to remain with your current carrier but update the terms of your program agreements to reflect your current operations. In other cases, a new carrier may be able to provide coverage more tailored to the new risks your company is encountering. Transitioning to a new insurer could have unintended consequences, however. The experience of your insurance advisor can be invaluable.

Should you choose to make a change, a strong relationship between you, your insurance broker, and the carriers will make the transition as smooth as possible.

Here are four ways your insurance broker can keep you informed about your choice of carrier to help you avoid any surprises.

1. Stay Ahead of New Market Conditions/New Insurers/New Coverages

Your broker can keep you apprised of factors impacting the overall market to prepare you for possible premium increases or decreases with your existing carrier well in advance of renewal. The broker should also be aware of insurers that are offering new lines of coverage and should approach the carriers for quotes on your behalf.

In addition, brokers can help you stay ahead of emerging coverages and potential exposures that may affect your business, which is critical to avoiding losses that may not be covered under your current policies. Understanding the differences among your policies, knowing what they do and do not cover, and advising you on what endorsements you should obtain for your standard policies can help ensure that your company isn’t exposed to unnecessary or avoidable risks.

Recently we worked with a new client to provide coverage for social engineering fraud (SEF), which occurs when a hacker imitating a senior executive, sends a phishing email to an employee telling the employee to wire company funds to a bank account on an emergency basis. The business owner mistakenly believed that either the cyber policy or the crime policy covered the loss. But neither of the policies had been endorsed to provide SEF coverage, and the business was left with a gap in coverage that the risk manager hadn’t realized until we brought it to the manager’s attention.

2. Update the Fine Print of Your Program Agreements

Most carrier agreements stipulate that in the event you transition to a different insurer, the collateral amount can be reset at the carrier’s discretion. If your policy is on a large deductible or other type of loss-sensitive program, you might experience substantial cost implications. Your broker can thoroughly review your program agreements with your insurers and, if possible, amend this wording by setting specific parameters around how the collateral will be calculated. For example, the calculation might include predetermined loss-development factors or consideration of the insured’s outside actuary calculations.

3. Review Outstanding Claims

When you change carriers, there will inevitably be outstanding claims to process, but standard agreements typically nullify any special claims-handling procedures that were put in place while you had your coverage with the insurer. As a result, you will still be dealing with claims, but you might lose the ability to have any or all of the following:

- Free claims reviews

- Use of a pre-selected defense counsel

- Notification of reserve changes

- Ability to have input on settlement amounts

- Continuity of adjusters because the insurer will most likely move any open claims to a different unit

Your broker should review the agreement around what happens if you move from the insurer and, when appropriate, modify the agreement to create as much certainty as possible around the way outstanding claims will be handled.

4. Adjust for Changes in Insured Operations

Many insurance policies limit coverage to events that occur in a certain geographic area. The insured area is often referred to as the “coverage territory.” If your company expands its operations outside the United States, your broker will need to review the coverage territory in all policies to ensure there are no exposures in your new areas of operation that aren’t covered in the existing policy. Similarly, if your company begins offering new products or expands on the scope of existing services, an in-depth review of your existing coverages is necessary to make certain no new coverage is needed.

Here are two examples of changes in insured operations that we’ve helped our clients with recently:

- An insured established a new 401(k) plan and began providing health coverage to employees. They now needed fiduciary liability coverage because these plans are subject to ERISA and present possible personal liability to plan administrator.

- An Insured decided to hire a sales force who will be driving on company business. After reviewing their options, they elected to increase the limits carried on their automobile liability coverage and added to their umbrella coverage limits.

Anticipating and planning for change is part of business. Don’t be lulled into a sense of complacency and simply renew with the same insurer year after year. You have options. Your broker is a trusted business partner who can help you actively avoid any of the potential insurance minefields that come with change, as well as choose the right path forward for your continued business success.

About the Author

Joe Tatum is the CEO of Relation Insurance Services, a premier insurance brokerage that offers risk-management and benefits-consulting services through its family of brands across the United States.

This article originally appeared on the PropertyCasualty360 website here and in a printed edition of National Underwriter.

Dear Clients,

With Hurricane Florence gaining in strength and intensity and due to hit the East Coast in a matter of hours, we urge all of you to make sure you have a plan in place and are prepared for the worst-case scenario, even if you or your business are in an inland county. Your safety and wellbeing are important to us and we want to let you know that we care and we are here for you during this storm.

To be available to YOU when you need us most, our Relation Storm Team will be working remotely with extended hours from 7am-7pm throughout the storm, starting Thursday, 9/13, and continuing every day through Monday, 9/17 (including Saturday and Sunday).

We will be available to take your calls and respond to emails and file any necessary claims as needed. We have also included direct claims reporting and payment information for our major insurance carriers below for your convenience to report your claim directly on a 24-hour basis.

If you are unsure of your carrier or policy information, you can call our main number at 704-688-1228 or 800-456-1696 or email us at [email protected] during our extended hours to assist you in getting your claim filed. During normal business hours, you may continue to reach out to your account manager as you do currently.

Florence is expected to be the most powerful storm to make a direct hit on the Carolinas in decades. Experts are expecting wide and significant impact to our area, no matter where it ultimately comes ashore. At the very least, we can expect Florence to bring heavy rain and wind which can easily cause flooding and power outages. There is additional concern due to the large expected area of impact and the extended time that it may stay in our area. Many of our client families and businesses are already under a mandatory evacuation with more on the way. If you are in an evacuation zone, please heed that warning and DO NOT attempt to stay in your home. If you are not under an evacuation order, there is still time to prepare. We have attached some storm tips as well as a blank emergency plan that might be helpful to your household in this process.

Our Coast is expected to feel the blast early tomorrow with damaging and life-threatening storm surge, wind and rain. In central areas, we expect to feel the impact due to sustained rainfall and significant wind. In western areas of our states, we should still be prepared for heavy and sustained rain that might trigger flooding and mudslides. Please stay alert and take this storm seriously no matter where you live in our Carolinas and East Coast states. If you are under an evacuation order, please heed that order. If you aren’t under an evacuation order, take this time to gather your supplies: food, water, flashlights, extra batteries, medications and important documents. Remember to make plans for your pets. Clear your yard of debris that can cause damage in high winds.

Both North Carolina and South Carolina have some great resources and mobile applications for your use in preparation for and during the storm:

The ReadyNC mobile app gives information on real-time traffic and weather conditions, river levels, evacuations, and power outages and is an all-in-one FREE tool for emergency preparedness. The SC mobile app can help you build your emergency plan, keep track of supplies and stay connected to loved ones. In addition, coastal residents can now “Know Your Zone” instantly using the maps feature as well as locate the nearest emergency shelters when they are open. The tools section features a flashlight, locator whistle and the ability to report damage to emergency officials.

Federal sites are also helpful, or download the FEMA mobile app for resources on how to plan and prepare for a hurricane event as well as steps to take afterward to minimize damage and to get back in business or back in your residence as soon as possible. You can also text PREPARE to 4FEMA (43362) to receive useful tips about how to prepare for disasters.

See the National Hurricane Center for updates on the storm and to the National Weather Service for detailed warnings.

Please be safe during this storm and reach out to us at any time with questions and concerns.

Other Helpful Resources

Personal Lines Claims Reporting Phone List

Personal Lines Direct Bill Payment Phone List

Commercial Lines Claims Reporting Phone List

Commercial Lines Direct Bill Payment Phone List

Relation Storm Tips

Household Emergency Plan

What to Take to a Shelter

19 Post-Florence Tips: What to Do After the Hurricane

By Steven J. Billings, Michael Williams, and Travis Vance

Safety incentive programs have long been used by organizations to promote safe working environments and to encourage safety in the workplace. But a recent memorandum from the Occupational Safety and Health Administration (OSHA) states that “Section 11(c) of the OSH Act prohibits an employer from discriminating against an employee because the employee reports an injury or illness. Reporting a work-related injury or illness is a core employee right, and retaliating against a worker for reporting an injury or illness is illegal discrimination under section 11(c).” Given OSHA’s recent scrutiny of incentive programs, discipline programs and drug testing post-incident, employers should take this opportunity to review their safety program to ensure its compliance with OSHA’s new rules.

Consider the following 10 tips to make your incentive program OSHA compliant and more effective:

- First, a safety incentive program should be behavior-based rather than being injury-rate-based. It means employers should provide incentives to workers practicing safe operating procedures and practices instead of incentivizing plans based solely on number of accidents.

- Reporting near misses, hazardous behavior and situations on the front end should be a point of focus, which will prevent future accidents and injuries. (Leading vs. Lagging Indicators)

- Praise and recognize employees through top management, in a timely manner, and in front of others to acknowledge their safe behavior and encourage others to act in the same manner.

- Monetary rewards are okay for safety programs as long as they are not based on “reporting an incident”. You can also utilize other rewards such as keeping points, safety bucks, certificates, days off, safety pins and recognition boards.

- Reward employees for a wide variety of safety activities such as providing safety suggestions to daily operating procedures, guiding a co-worker or new hire to perform a task safely, identifying a hazard or participating in safety committees.

- Programs cannot be vague or limited to the actual reporting of an incident. “No injuries reported” or “Acting Safely” is not a safety incentive program, as these metrics give clear motivation for employees not to report injuries, or they are unclear as to what needs to be done in order to qualify. Direct incentives based on employees behavior, and the qualifying metrics/procedures should be documented clearly. A basic example would be “drivers must be on time every day, turn in all paperwork on time, follow all company outlined safety procedures and day to day tasks as outlined in the fleet safety manual to qualify for our company incentive plan”.

- Make sure your safety program is robust and clear, outlining how you want your employees to conduct themselves and how you want them to perform the key elements of their job (3 points of contact getting in and out of truck, using all required PPE, wearing hard hat at jobsites, observing and following all posted road/traffic signs, not following too closely, observing smith system rules, etc.).

- It is vital to incentivize/discipline all employees equally. If you observe someone not following a company safety procedure, but no incident occurred, they should be disciplined the same way as someone not following the same safety procedure that led to an accident. The accident/incident is the byproduct. What we want to do is applaud/discipline the behavior/action, not the end result, evenly across your workforce. This also requires management/supervisors to be engaged and actively observing all the time.

- Ensure management commitment by demonstrating that organizational leaders care about safety. This can be done by having them give presentations and establish safety as a core value of the company, believing that all injuries are preventable, and having zero incidents is possible.

- Allow employees to set safety goals for themselves. This will motivate them to ensure their own commitment to safety and work towards achieving it.

The Bottom Line

Adopting these suggestions will empower your safety program, help minimize incidents and at the same time prevent OSHA violations. To make things easier, think as if you are an employee working for your company. Does your plan incentivize you to become more safety focused, or afraid of the repercussions of reporting an incident or injury? If the answer is the latter, then refocus your efforts in going through the 10 suggestions listed above, and find a partner that is well versed in safety incentive plans to help guide you.

By Joe Dunn, Angel Mendez, and Scott W. Dunn

Agribusiness clients are acutely aware of the high premiums they pay for workers’ compensation, premises liability, health insurance and the steps they can take to mitigate those costs. On the other hand, automobile liability has historically been a low-cost, low-visibility afterthought. Not anymore.

The risk associated with catastrophic vehicle-related losses is on the radar of underwriters who insure agricultural operations.

Many have seen loss ratios spike to 90 percent or higher on their auto liability book of business and are alarmed by the skyrocketing frequency and severity trends. In an informal poll, agricultural insurers expressed concerns that the market for auto coverage is seriously underpriced, and some are considering rate increases as high as 30 percent. Said one underwriter, “If you can’t get enough rate, you just have to walk away from some accounts.”

Consider the following scenarios:

- As he does every day, a California farm labor contractor transports employees to and from job sites. One evening, while driving six workers home, the contractor drifts off the highway. He overcorrects, causing the van to flip several times. All six passengers, including two underage girls, are ejected from the vehicle. Three men are pronounced dead at the scene and one of the underage girls later dies from her injuries.

- After inspect-ing a field to be harvested, a farm labor contractor employee stops at a bar and consumes five shots of whiskey and two 22-ounce beers in a three-hour period. He subsequently climbs into his truck and, while texting, rear-ends a car stopped at a red light. A four-year-old boy in the rear-ended car is killed instantly, while his mother and sister are injured.

Catastrophic vehicle losses have a significant impact on the agribusiness industry and create turmoil for both insureds and insurers. The emotional and financial toll in the case of a death or severe disability resulting from a vehicular accident can affect victims and their families forever. Employers dealing with vehicle-related claims involving their employees also face the devastating financial consequences of insured and uninsured costs increasing exponentially.

The insured costs most likely to be impacted arise from automobile liability, umbrella/excess liability, workers’ compensation and employers’ liability policies. Insureds typically have deductibles, or self-insured retentions and claim costs will need to be paid. In the longer run, a poor motor-vehicle or employee-injury-loss history can result in premium increases, mid-term cancellations, or worse yet — the unwillingness of any carrier to quote the account. Uninsured costs, including the following, are frequently overlooked but can be even more costly:

- Lost production time;

- Damage to crops/other products;

- Increased overtime for existing employees;

- Loss of experienced staff;

- Need to hire and train new/temporary labor;

- Damaged employee morale;

- Investigation and legal expenses;

- Governmental agency audits/fines;

- Loss of management’s time; and

- Negative publicity.

The risk associated with catastrophic vehicle-related losses is on the radar of underwriters who insure agricultural operations.

According to the National Highway Traffic Safety Administration (NHTSA), 2016 was a deadly year on the roads with 37,461 deaths — a 5.6 percent increase over the number of deaths in 2015. In addition, vehicle crashes are the leading cause of work-related deaths, accounting for 24 percent of all occupational fatalities, according to the National Safety Council.

The silver lining in the NHTSA study is that more than 94 percent of accidents are caused by human error and are thus preventable with proper training.

For employers, the best preventative tools are careful driver recruitment and comprehensive driver and fleet safety education. The “gold standard” of driver training is the National Safety Council’s Certified Defensive Driver Courses, which are available in either a classroom setting or online. For employers that are unable to commit their workforce to the time and expense of an intensive certificate program, insurers and broker loss control and claims consultants can tailor short “tailgate talk” training sessions that focus on, amongst other things, the following topics:

- Driver-selection tips;

- Drug-and-alcohol testing protocols;

- MVR-review policies;

- Defensive-driving techniques;

- Cell-phone usage;

- Vehicle inspection and maintenance;

- Accident response and investigation procedures;

- Post-loss claim-mitigation strategies;

- Driver-incentive and discipline programs; and

- Mock DOT and OSHA audits.

Employers’ negotiating positions on auto liability, umbrella/excess and workers’ compensation program renewals are strengthened when they can demonstrate to underwriters the tangible steps they have taken to become a better-than-average risk. The potential return on investment? Objectively, a well-designed safety program that has achieved meaningful reductions in auto and employee injury claims can yield the following financial benefits:

- Increased competition for the account as underwriters vie for quality risks.

- The ability to effectively counter upward premium pressures.

- The confidence to increase deductibles or retentions, thus lowering premiums.

Subjectively, employers will have a safer workplace and more contented workforce.

The farm labor contractor from the first scenario did not have a driver’s license and ended up being sued by multiple parties. He filed for bankruptcy and ultimately went out of business. In addition, the U.S. Department of Labor sued the grower that hired him for violating worker safety and transportation laws.

The alcohol-impaired driver from the second scenario was sentenced to a mandatory 16-year prison term for gross vehicular homicide. His employer’s auto and umbrella liability coverage ended up paying out a multi-million-dollar settlement.

This whitepaper was featured in Insurance Journal’s Workers’ Compensation Newsletter on March 1, 2018 and published as an eMagazine on February 19, 2018.

Joe Dunn is the claim services manager, Mendez is a senior loss-control consultant, and Scott W. Dunn is vice president/risk advisor specializing in agribusiness, all of Pan American Insurance Services, a Relation company.

SF Biz Times Exclusive: Startup Zendrive to triple workforce at new San Francisco headquarters

Transportation data company Zendrive this month moved into a new office to expand its San Francisco operations and says it wants to triple its workforce here.

The company analyzes mobile phone data to predict driving behavior and helps insurers identify risky drivers. Its customers uses these analytics to manage their vehicles, drivers and liabilities.

Zendrive charges enterprise customers a fee per driver monthly and earns commissions through its insurance agency ZD Insurance Services, LLC. The affiliate acts as an agent for its insurance partners.

By using smartphones to track cars and driver behavior on the road, Zendrive works with insurance companies and transportation planners to lower their costs and collisions using data analytics. It is building out a new headquarters with 7,500 square feet on the third floor of 929 Market St. to triple its workforce. The company has 61 employees in San Francisco and Bangalore, India, with most of the anticipated growth here.

Distracted phone use causes a quarter of car accidents in the U.S., according to the National Safety Council. Zendrive said its technology and data can improve driver safety by collecting data on behavior, like speeding and hard braking, and phone use. The company said it is amassing data on tens of millions of drivers and tens of thousands of crashes but keeps the data anonymous and does not share with anyone.

These insights could affect how auto insurers set their prices and help transportation businesses learn more about what causes accidents, where they happen and types of drivers who cause them, Zendrive said. However, the startup said it doesn’t directly report data to insurance companies, and it cannot identify drivers, their companies or insurance from their data.

Zendrive has raised about $20 million in funding, backed by investors including First Round Capital and BMW iVentures. It was founded by Jonathan Matus and Pankaj Risbood in 2013 to focus on using data analytics to improve road safety. Matus, who spent several years at Google then Facebook working on mobile products, said he felt responsible for working on smartphone technology that added to people’s distractions on the road.

“I didn’t feel that was a meaningful use of the people around me and the use of my time,” said Matus, founder and CEO of Zendrive.

Smartphones were killing people, but they could also be used to save their lives, Matus said. So Zendrive has created a developer platform for companies to analyze driver behavior in order to prevent accidents and develop insight on their fleets.

Using smartphone sensor and GPS technology, it captures data around collisions, distracted driving and aggressive driving and then sends driver coaching insights and recommendations through its dashboard, an API, emails or text alerts. The app scores drivers’ performance and sets goals for them.

Zendrive said its driver coaching, which costs $4 per driver per month, can help reduce crashes by up to 49 percent, and the tool will get better as it accumulates more data. On average, the company analyzes more than 15 billion miles of data every two months, totaling about 50 billion miles so far.

That’s compared to Progressive Insurance, for example, which in 2017 reported collecting 15 billion miles of data over 18 years, Matus said.

“We’re going to hit 100 billion (miles) soon,” he added.

Zendrive will continue growing its team in India, which occupies a large building with two floors and will add two additional floors. The company has also been working with autonomous vehicle partners to research safety and road conditions in that upcoming market.

Using insightful data to determine prices has caught on in the business. Insurance company Metromile, also based in San Francisco, is using a small GPS device installed in customers’ cars to bill based on usage, and the company raised some $150 million in 2016 alone. It now has more than $200 million in funding, according to Crunchbase. It is available in seven states and expanding service to New York, Texas and Florida.

Tom Pataluch, director of software development at Walnut Creek-based Relation Insurance Services Inc., said these technological changes have enabled insurers and businesses to look beyond aggregated data, which traditionally included information like driving history and deductibles. Now they can collect more personal history and data in real-time to come up with more accurate rates.

“Data is becoming increasingly important. I can definitely see cases where it can help companies with fleets and the trucking sector to manage risk,” Pataluch said.

But not everyone will see savings on Zendrive. Rates are still tied to driver behavior: Drivers going slower on shorter trips will see rates go down, and drivers going faster over longer distances might see rates go up.

“It will lower the rates for some and increase the rates for others,” Pataluch said.

This article, authored by Antoinette Siu, originally appeared in the San Francisco Business Times on January 22nd, 2018.